UPI Plus WhatsApp Is the Whole Checkout

In India, paying is the easy part. With UPI behind almost every digital payment, chat ordering plus a UPI link removes the last friction in direct restaurant ordering.

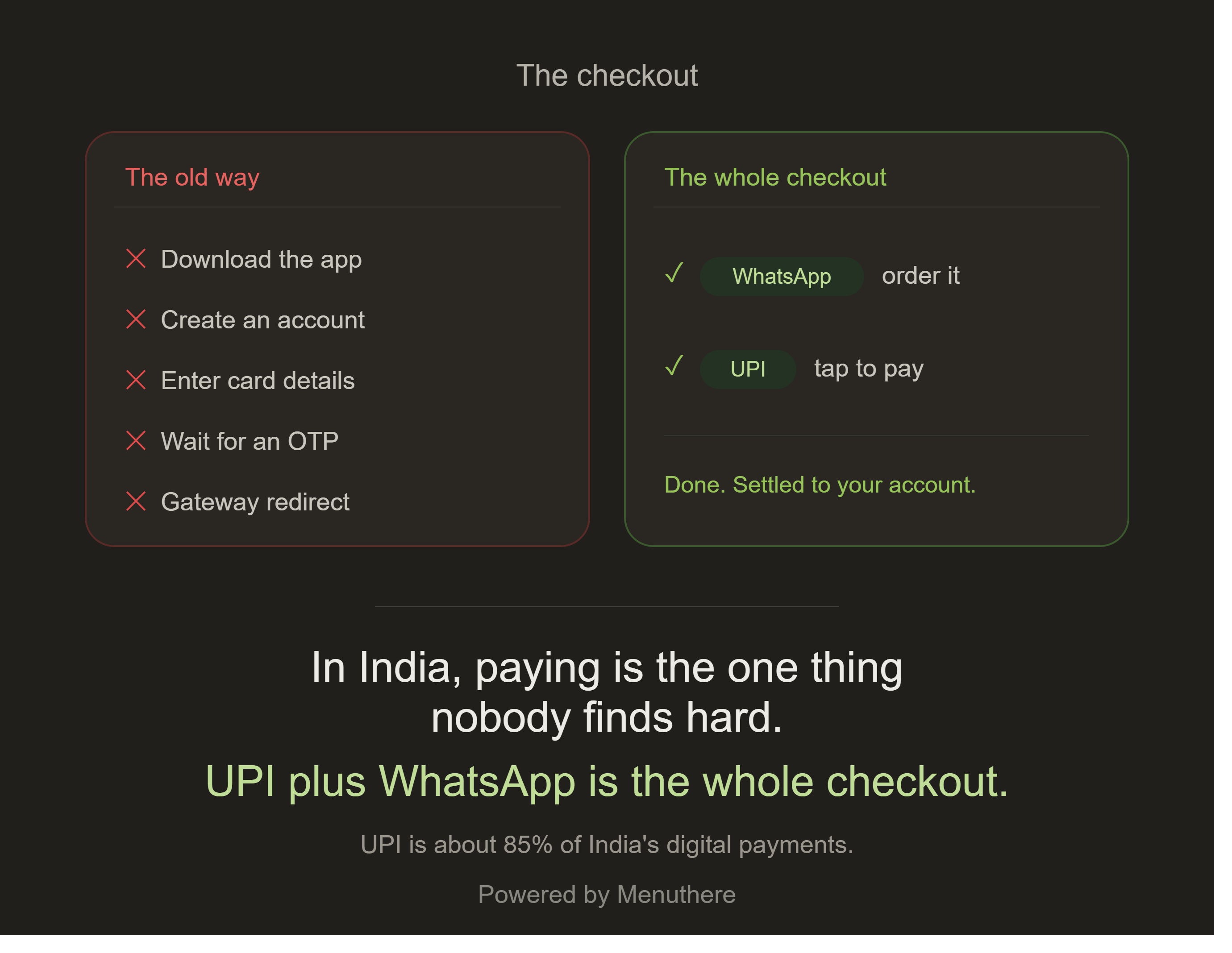

For years, the real friction in ordering food was never the menu. It was the checkout. Download this app, create an account, type in a card number, wait for an OTP, get bounced to a payment gateway, watch the loading spinner, hope it does not fail. Every one of those steps was a place to lose a hungry customer who just wanted dinner.

In India, that entire problem is already solved, and most restaurants have not noticed. Paying is now the single easiest thing an Indian customer does. UPI handles close to 85 percent of the country's digital payment volume, running about 66 crore transactions a day, and it just crossed a record ₹29.90 trillion in a single month. The infrastructure for a frictionless checkout is not coming. It is already in every customer's pocket, and they use it dozens of times a week.

The checkout was the friction, and it is gone

Think about what the old digital checkout actually demanded. A new app on the phone. A new account and password. Card details typed on a small screen. An OTP from a different app. A redirect to a gateway that sometimes timed out. Each step shed customers, and the ones who pushed through did it grudgingly.

Now look at how an Indian pays for anything today. They open an app they already have, scan a code or tap a link, approve with a fingerprint, and it is done in seconds, with a success rate above 99 percent. There is no new account, no card to fetch from a wallet, no gateway to fear. The hardest part of the old checkout, payment, has become the easiest part of daily life.

That changes the whole equation for ordering. If paying is effortless, the only thing left to remove is the ordering, and that lives perfectly well in a chat.

The whole checkout, in two things people already do

Here is the insight that should reshape how restaurants think about direct ordering. The complete checkout now collapses into two actions every customer already performs daily, with no learning curve at all.

They chat on WhatsApp. And they pay on UPI.

So the flow becomes almost absurdly simple. The customer places the order in a WhatsApp conversation, the way they already message a shop. They receive a UPI link or a dynamic QR for the exact amount. They tap, approve, and the money lands in the restaurant's account. The confirmation comes back in the same thread. No app to download, no account to create, no card to type, no gateway to redirect through. Two familiar habits, stitched into one seamless order.

You are not asking the customer to adopt anything new. You are connecting two things they already do without thinking.

Why this is an India advantage, not a generic one

This is not a tactic that works everywhere. It works extraordinarily well in India specifically, because the rails are uniquely built for it. Merchant payments already make up 63 percent of UPI volume, and 86 percent of those are under ₹500, which is almost exactly the shape of a typical food order. Fast food is already one of the largest UPI merchant categories by value. The behaviour, the ticket size, the trust, all of it is already in place.

In other words, the hardest and most expensive part of building a direct ordering channel, getting people comfortable paying you directly, is a problem India solved years ago. Restaurants just have to plug into it instead of routing customers through an app and a card gateway as if it were still 2018.

The cost kicker

There is a margin story buried in here too. A card payment through a gateway typically costs a restaurant around 2 percent. An aggregator takes around 30 percent. UPI, for most merchant payments, costs close to nothing. So when the checkout runs on UPI, the payment cost on a direct order shrinks toward zero, which is the quiet reason a direct channel is so much cheaper to run than the alternatives. The same order that loses a third of its value on an aggregator keeps almost all of it when the customer chats to order and pays by UPI.

The playbook

1. Stop sending people to an app or a card gateway

Every redirect is a place to lose the order. If your direct ordering still pushes customers into a separate app or a card form, you are recreating the friction UPI already removed.

2. Take the order where the customer already is

Let the order happen in WhatsApp, the chat they already trust and already have open. The menu and the order live in the conversation, not behind a download.

3. Send a UPI link or a dynamic QR for the exact amount

Close the order with a UPI request for the precise bill. One tap, fingerprint, done. No typing, no OTP juggling, no spinner of doubt.

4. Settle straight to your account

UPI lands the money directly with near zero fee. No gateway cut, no aggregator commission, no waiting on a platform payout cycle.

5. Confirm in the same thread

The order, the payment, and the confirmation all live in one WhatsApp conversation, and the customer's number is saved for the next order. The checkout and the relationship are the same flow.

6. Watch your completion rate

Track how many started orders actually get paid. When you remove the app and the card form, the share of orders that complete tends to jump, because nothing is left to trip the customer up.

The bottom line

The objection to direct ordering used to be that payment was too hard without an app and a gateway. In India, that objection is dead. UPI has already taught the entire country to pay in one tap, and WhatsApp has already taught them to order in a chat. The two together are not a workaround. They are the whole checkout.

Menuthere is built on exactly this. Your QR menu becomes a WhatsApp ordering channel, the order is placed in chat and paid by UPI, and the money and the customer both stay with you. The hardest part of selling direct was always the checkout. India already built it. Use it.

The whole checkout, in two taps. Menuthere turns your QR menu into a WhatsApp ordering channel with UPI payment built in, so customers order in a chat and pay in a tap.

Sources: NPCI and PIB 2026 UPI statistics on transaction volume, value, merchant share and ticket size, IMF recognition of UPI as the largest real time payment system, and Restroworks data on digital payment adoption in Indian restaurants.